Why India’s CAG Needs Appointment Reform to Protect Its Independence

CAG Office India (Image official website)

By P. SESH KUMAR

India’s Constitution gives the CAG extraordinary protections after appointment but leaves the selection process almost entirely to the executive. As multiple petitions reach the Supreme Court, this opinion piece examines whether the nation’s top auditor can remain truly independent without reforms to how the officeholder is chosen.

New Delhi, July 5, 2026 — The Comptroller and Auditor General of India (CAG) is, on paper, among the most fortified offices the Constitution conjured into being–Babasaheb Ambedkar called the holder “probably the most important officer” under it, ranked equal to judge of Supreme Court. Yet the fortress has one wide-open gate. The Constitution armours the CAG on the way out–removal only by parliamentary impeachment, salary charged on the Consolidated Fund, a lifetime bar on further office–while leaving the way in entirely unguarded: no qualifications, no eligibility, no selection committee, no published criteria. A retiring bureaucrat is simply handpicked by the Prime Minister and waved through by the President.

The Cathedral (or Temple) and the Unlocked Door

When B.R. Ambedkar defended the office of the Comptroller and Auditor General (CAG) in the Constituent Assembly, he called it “probably the most important officer” under the Constitution, underscoring its role as the guardian of the public purse. To safeguard its independence, the Constitution gives the CAG protections comparable to those of a Supreme Court judge. Under Article 148, the CAG can be removed only through an impeachment-like process for proved misbehaviour or incapacity. Article 149 empowers Parliament to define the CAG’s duties through the CAG Act, 1971, while Article 150 gives the office authority over the format of government accounts. Article 151 requires the President and Governors to place CAG reports before legislatures, preventing the executive from suppressing audit findings. The CAG’s expenses are charged to the Consolidated Fund of India, insulating the office from annual budget votes. To preserve impartiality, Article 148(4) bars a retiring CAG from holding any further government office.

It is, in short, a cathedral or temple built to keep the executive out. And it has one unlocked door.

While the Constitution heavily safeguards the CAG’s independence after appointment, it is strikingly silent on how the officeholder should be chosen. Article 148(1) merely states that the President appoints the CAG by warrant under his hand and seal, prescribing no qualifications, eligibility criteria, consultation or selection process. This vacuum has allowed the executive to establish a convention in which the Cabinet Secretariat shortlists candidates, the Prime Minister selects one, and the President formally appoints them. In practice, the government appoints the official responsible for auditing its own finances, usually choosing a retiring senior bureaucrat from within the executive.

Three Petitioners at the Gate

That asymmetry is now the subject of not one but three live challenges in the Supreme Court, and they have begun to converge.

The challenge to the CAG appointment process reached the Supreme Court in January 2024, when Anupam Kulshreshtha and others argued that the absence of a statutory selection procedure had created a “legal vacuum.” They contended that the Cabinet Secretariat effectively controls appointments by shortlisting candidates without transparent criteria, allowing the executive to choose the government’s own auditor. A Bench led by then Chief Justice D.Y. Chandrachud issued notices to the Law and Finance Ministries. The petition relied heavily on the Supreme Court’s 2023 judgment in Anoop Baranwal v. Union of India, which held that security of tenure alone cannot ensure institutional independence and introduced a new appointment mechanism for Election Commissioners. The judgment also noted that the CAG, like the Election Commission, lacks constitutional or statutory appointment criteria. Senior advocate Prashant Bhushan, who argued Baranwal, also appeared for the CAG petitioners, reinforcing the constitutional parallel.

In March 2025, the Centre for Public Interest Litigation, represented by Prashant Bhushan, challenged the CAG appointment process, arguing that executive control violates Article 14 and the Constitution’s basic structure. It sought a selection committee comprising the Prime Minister, the Leader of the Opposition and the Chief Justice of India. Bhushan argued that the CAG’s perceived independence had eroded, citing fewer audit reports and alleged delays in auditing Maharashtra before Assembly elections. The Supreme Court issued notice but cautioned against undermining institutions, observing that the Constitution itself vests appointment power in the executive. The case was tagged with the earlier petition.

The third is the most pointed. In August 2025 the NGO Lok Prahari moved the Court not merely against the process but against the person–questioning the appointment of the sitting CAG, K. Sanjay Murthy, and demanding a transparent mechanism to install a “politically neutral” holder. Murthy’s elevation in November 2024 had itself raised eyebrows: a 1989-batch IAS officer then serving as Secretary, Higher Education, who was weeks from superannuation and instead vaulted into a five-year constitutional term. There was also the moot point whether at all, CAG would conduct the performance audit of National Testing Agency with regard to recent NEET paper leaks. Three petitions, one grievance: that a watchdog chosen entirely by those it must watch can never quite shake the suspicion that it was bred to heel.

The Auditor in the Dock

If anyone doubts that the choice of CAG can come back to haunt the institution, the case of Shashi Kant Sharma should settle it.

Shashi Kant Sharma’s career illustrates the conflict-of-interest concerns surrounding the CAG’s appointment. A 1976-batch IAS officer, he served as Defence Secretary from 2011 to 2013 after holding key acquisition roles, including overseeing decisions linked to the AgustaWestland VVIP helicopter deal. He was later appointed CAG—the very authority whose 2013 audit sharply criticised the procurement process. This meant the official associated with approving the deal headed the institution responsible for auditing it. The CBI sought sanction to prosecute Sharma only in 2020, three years after his CAG tenure ended. A supplementary charge sheet followed in 2022, and a special CBI court took cognisance before granting him bail; the case remains pending. When the appointment was challenged, the Supreme Court invoked the “doctrine of necessity,” holding that a single-member constitutional office could not recuse itself, highlighting a structural gap rather than resolving it.

Mutiny in the Audit House

The ‘presidency’ of Girish Chandra Murmu (2020–2024) supplied a different, and in some ways more disquieting, spectacle: not executive capture from without, but the charge of arbitrary power from within.

In August 2024 a nearly 6,000-word complaint from what called itself “a cohort of vigilant employees” of the CAG’s office landed on senior desks, levelling grave allegations–corruption and sexual misconduct–against a 2010-batch Indian Audit and Accounts Service officer, including possible misconduct during an audit assignment in Mauritius and bribery in recruitment. Some said it was all due to internal bickering and ‘politics’ by disgruntled elements within the establishment.

What happened next is what turned an internal complaint into an institutional embarrassment. Despite the allegations, he was allowed to take charge of a plum foreign posting–Director in the office of the Principal Director of Audit, London–in September 2024. Crucially, this was not a silent lapse: An Additional Deputy Comptroller and Auditor General, formally urged a preliminary inquiry on 28 August 2024, arguing the complaint could no longer be treated as anonymous (the complainant had attached his Aadhaar) and that, to be credible, the fact-finding committee must exclude the very wings and personnel named. The appeal was overridden.

Only when pressure mounted was the officer recalled in October 2024 “on administrative grounds,” reassigned to Jaipur, and finally suspended on 19 November 2024–a single day before Murmu’s own tenure concluded. He has, by mid-2026, spent the better part of two years under suspension, the inquiry grinding on. In a parallel episode, a Director General of Audit accused of falsifying travel claims during a Washington posting was, sources say, handed a ‘clean chit’ shortly before retirement of Murmu.

When senior auditors must put their objections in writing against their own chief–and lose–the rot is no longer about who appointed whom. It is about whether the institution can audit itself. An office that cannot apply its own propriety standards inside its own corridors forfeits some of its moral authority to apply them to anyone else.

The Great Shrinkage

Rajiv Mehrishi’s term (2017–2020) is remembered less for any single scandal than for a quiet, cumulative subtraction: the steady disappearance of the CAG and impactful all-India performance audits from public life.

The CAG’s declining output is reflected in the numbers. Under Shashi Kant Sharma, the office produced 150 audit reports in 2016–17, including 49 on the Union government. Under Rajiv Mehrishi, the figure fell to 98 and then 73, while by 2023 only 18 Union reports were tabled in Parliament, down from an annual average of about 40 between 2014 and 2018. Meanwhile, the Indian Audit and Accounts Department’s budget fell to about 0.13% of the Union Budget, alongside shrinking staff strength. Supporters argue the shift reflects a focus on fewer, higher-quality audits, but critics point to long delays, excessive scrutiny of draft reports and the redacted Rafale audit as evidence of growing caution. More significantly, the CAG has largely retreated from sweeping policy audits—such as the 2G and coal block reports—that once scrutinised government decision-making and shaped national political debate.

National Geospatial Policy 2022: Gaps & the Case for CAG Audit

The Geometry of Zeal

There is a pattern critics find hard to unsee: that the institution’s surviving energy seems unevenly distributed across the political map.

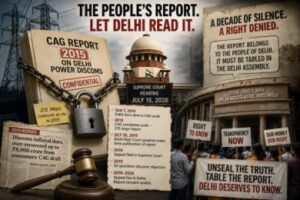

The sharpest exhibit is Delhi. Fourteen CAG reports on the Aam Aadmi Party government–covering state finances, public health, vehicular pollution, liquor regulation and the transport corporation–were not tabled during AAP’s tenure, surfacing only after the BJP took the Assembly in February 2025, whereupon the liquor-policy report alleging some Rs 2,000 crore in revenue loss became an instant political cudgel. In Maharashtra, an October 2023 headquarters communication is supposed to have made the Accountant General pause all field work on performance and thematic audits “with immediate effect till further orders,” a stoppage the CAG’s office denied having ordered even as the paper trail suggested otherwise.

Honesty requires the counter-reading, and it is a real one. The Delhi reports were withheld by the AAP government itself, and it was the Opposition of the day, with the Lieutenant Governor, that demanded their tabling–so the same episode can be read as the audit machinery being weaponised by and against whichever party holds the floor. That ambiguity is exactly the problem. When the timing of a report can be choreographed to an electoral calendar–whoever does the choreography–the audit ceases to be a neutral instrument of accountability and becomes another lever in the partisan tug-of-war. The CAG’s value was always that it stood outside that ring. The perception that it has stepped inside, even occasionally, is corrosive regardless of which corner benefits.

West Bengal offers the mirror image of Delhi, and an even starker one. Year after year the Accountant General’s office in Kolkata kept turning out audits on the Mamata Banerjee government–finance, panchayats, urban bodies, education–only to watch them vanish into a drawer, because a state’s reports reach daylight solely when the government of the day consents to lay them before the Vidhan Sabha.

The last report actually tabled covered 2020-21; four full years of findings–2021-22 through 2024-25–were bottled up, marinating out of public view even as the Governor pressed for their release. And the buried numbers were no trifles: utilisation certificates worth roughly Rs 2.29 lakh crore had gone unsubmitted between 2011 and 2020–the Panchayat and Rural Development Department alone accounting for some Rs 81,839 crore-alongside Rs 3,400 crore of abstract contingent bills never squared with detailed accounts, the auditor warning bluntly that such gaps invite misappropriation and embezzlement.

When the CAG’s 2020-21 findings did surface, the state took the extraordinary step of branding a constitutional auditor’s report “erroneous,” with the Chief Minister writing to the Prime Minister to say so–reportedly the first time a state government had called a CAG report outright wrong. The coda writes the moral in neon: with the BJP now in power in West Bengal, the very reports the TMC had smothered are being marched into the Assembly as political ordnance–proof, once again, that a withheld audit is not accountability deferred but accountability weaponised.

The MoU Carnival

The current CAG’s tenure has been marked by a series of memorandums of understanding (MoUs) with institutions including IIT Madras, IIM Ahmedabad, IIM Kozhikode, IIM Mumbai, the National Institute of Urban Affairs, the Digital India Bhashini Division, the Janaagraha Centre, and even the Central Board of Direct Taxes (CBDT), an entity the CAG audits. These partnerships are presented as efforts to strengthen capacity, AI-driven auditing and support the “Viksit Bharat 2047” vision. While collaboration and technological modernisation are legitimate goals, critics question the constitutional propriety of the CAG partnering with executive agencies it is meant to scrutinise. None of the MoUs publicly sets out measurable deliverables or expected outcomes. Critics argue the emphasis on institutional tie-ups contrasts with declining audit output and risks prioritising publicity over performance. Some insiders also see the collaborations as reflecting diminished confidence in the CAG’s own professional expertise, particularly when audited entities are expected to train the constitutional auditor itself.

The Reckoning

If we strip away the individual scandals, a single structural truth remains: the CAG is protected from everything except the one thing that matters most. It is shielded from dismissal, from financial coercion, from post-retirement temptation–and exposed, totally, at the moment of selection. Every controversy in this note flows from that unlocked door. Sharma walked through it from the Defence Ministry. The shrinkage, the redactions, the choreographed timings, the MoU carnival–all are downstream of an office whose every occupant owes his chair to the executive’s unbounded discretion.

The fixes are neither novel nor radical. The Second Administrative Reforms Commission long ago urged a bipartisan, multi-member selection body with a defined role for the Opposition; Anoop Baranwal supplies the template the petitioners now invoke. Prescribe qualifications. Publish the shortlist and the reasons, as the Court already requires for Information Commissioners. Take the sanction to prosecute senior officials out of the hands of the government that appoints them. Restore the all-India performance audit as a duty, not a discretionary luxury, and put audit output and tabling timelines beyond executive choreography. And reconsider whether a single-headed constitutional auditor–forever unable to recuse itself–was ever the right design for a body that has to almost every other day, audit the files its own chief once signed.

Ambedkar thought the auditor is the most important officer in the Constitution. He built a magnificent cathedral and forgot to lock the front door. Until that door is fastened — by Parliament, or failing that by the three benches now seized of the question — India’s supreme audit institution will remain what this season has revealed: a watchdog of formidable pedigree and uncertain appetite, superbly armoured against being thrown out, and quietly grounded by the manner of how it gets in.

(This is an opinion piece. Views expressed are the author’s own.)

India’s Grassroots Audit Crisis: Why the CAG Must Reclaim Oversight

Follow The Raisina Hills on WhatsApp, Instagram, YouTube, Facebook, and LinkedIn